Quick Auto Talk (12/10/19): The Average Auto Loan Payment For New & Used Cars In Every State

There’s no question that the cost of buying a car is going up across the board. Vehicle prices are higher, loan amounts are greater, and the terms are longer than ever. With that said, we wanted to see what people were paying in each state for both new and used cars, and what that data might reveal.

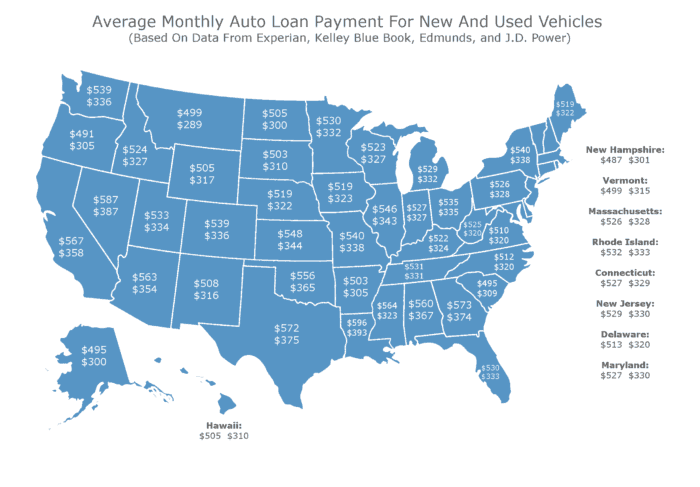

The map above is based on data from Kelley Blue Book, Edmunds, J.D. Power, and Experian.

As you can see, the states in the south having the highest auto loan payments, and often times this coincides with the average credit rating in the state. In addition, many of the states with the lowest auto loan payment do not have state sales tax on vehicles, in addition, the average credit score for those states is on the higher end of the spectrum (New Hampshire, Oregon, Delaware, Montana, Alaska).

Texas is an especially interesting case, as they have led the nation in overall auto debt for the entire decade.

The states with the highest auto loan payments are as follows:

1. Louisiana

2. Nevada

3. Georgia

4. Texas

5. California

6. Mississippi

7. Arizona

8. Alabama

9. Oklahoma

10. Kansas

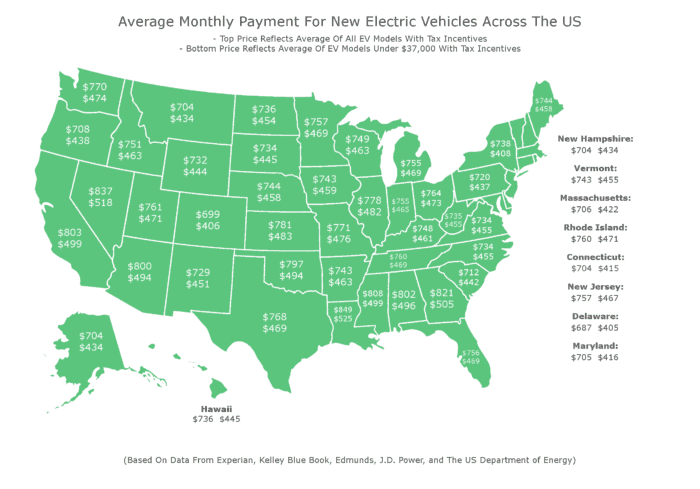

Update: The Average Auto Loan Payment For New Electric Vehicles (All Models and Models Under $37,000)

We decided to extend this study and specifically focus on Electric Vehicles. Our findings show that, on average, purchasing a new EV will cost significantly more than a standard new car… reason being, the average cost of a new electric vehicle is currently around $55,600. However, if we look at EVs that are priced in line with the average cost of a new gas powered vehicle, we see that EVs are currently cheaper to buy because significant federal and state tax incentives are still in effect (the exception being most Telsa Models, as the incentive for them will run out completely in 2020).

______________________

Everyone wishes they could walk into a car dealership with a briefcase full of cash, slap it down, and drive off in a new vehicle within 10 minutes. Unfortunately, that’s not the reality for most of us, so we have to get a loan.

Many consumers tend to spend days making sure they get the best price on a car; however, they neglect to shop around when it comes to the best car loan. This is a huge mistake.

If you are a car shopper who does not have adequate financing when you visit the car dealership to purchase, you are vulnerable to the terms that the dealer offers. These terms may have a steep interest rate and can put you at a disadvantage. And since dealers usually mark up their interest rates on a loan above what you actually qualify for, you could end up spending hundreds or even thousands of dollars more over the term of your loan.

In case you are looking to buy a car, this is a great time to score the best deal – not just on the price of your car; but also on a car loan. Due to the emergence of a number of online lenders, especially over the past few years, the competition to offer customers with auto financing has become fierce.

Nowadays, there are several different options for auto loans. So, finding the best rates on your car loan must be the first step in your car buying process.

Keep in mind that the most suitable car loan for you will depend largely on your priorities; that being said, two common and important goals are getting the most competitive interest rate as well as the lowest monthly payment.

This is the reason why longer-term loans have increased in popularity right now, and more and more buyers are stretching out used and new car loans over sixty months or even more. It is also worth noting that new and used auto loan payments reached an all-time high previous year, which means that individuals are spending a lot more on their car purchases. This is why we have compiled a comprehensive list of the best car loan providers in 2018.

We fully know and understand that with increasing rates, you will need help to find the lowest rates possible to secure the car you need and want. We took several factors into account when coming up with this list which include credit requirements, interest rates, vehicle restrictions, and loan terms.

Best Online Car Loan Services

Today, a lot of best car loan companies are not banks; rather, they are alternative lenders or non-banks spawned by the internet, especially after the banking debacle in 2008.

In the last five years these online lenders have proliferated, offering customers an entirely different auto loan shopping experience – an easy and swift application and approval process, highly competitive rates and fast funding.

LightStream is one of the most innovative and unique online lenders. As a qualified borrower, you can avail the company’s unsecured personal loans for almost anything. LightStream offers both unsecured and secured loans for all types of vehicles –used or new – whether you purchase from a private seller or dealer. You could get some of the lowest loan rates good to excellent credit.

Secured loans are usually provided to borrowers who have less than excellent credit. It is likely that you would require a minimum credit score of 660 in order to qualify for LightStream’s loans. LightStream provides loan terms ranging from 24 to 84 months with loan amounts in the range of $5,000 and $100,000.

The main downside is that the company is quite picky about customers. So, apart from excellent to good credit, you will have to prove a healthy income as well as assets in order to be approved.

LightStream Pros

- No fees

- Lowest rates you can find

- No restrictions on age and type of car

- It is possible to have same day approval and funding

- Secured loans available for borrowers with less than great credit

LightStream Cons

- Even a minor credit blemish may disqualify you

- It is not ideal for people who are seeking a conventional brick-and-mortar experience

MyAutoLoan can also connect you with lenders for almost all major types of car loans. It has the extra bonus of allowing loan applications for lease buyouts. You have to submit just one application and within only a matter of minutes you will receive as many as four offers.

In case you have excellent credit, you can currently avail the lowest car loan rate of about 1.99%. On the other hand, folks with less than excellent credit may get offers up to 24.9% (or 29.9% in case of refinancing).

Keep in mind that MyAutoLoan is an excellent source of finance for people who are looking to buy cars from private sellers or who would like to buy their leased vehicle. That being said, MyAutoLoan restricts its loan services to vehicles with a value of $8,000 or more, with less than 125,000 miles and which are less than ten-years old.

A convenient interest-rate estimator will help you get a rough idea of the amount you will have to pay on a car loan depending on your location, credit score and type of loan.

So, for instance, if you are looking at a new auto loan of $25,000 in Knoxville, Tenn., and have excellent credit, you may expect an average APR of about 3.11%; however, if you are looking at the same auto loan in Los Angeles, CA and have average credit, your average APR will be about 7.42%.

MyAutoLoan Pros

- Excellent resource, especially for first-time buyers

- No application fees

- The company offers financing for both private transactions as well as leased vehicles

- Offers financing options for individuals who have bad credit

- Quick turnaround time on the pre-approval process

MyAutoLoan Cons

- Your monthly income should be at least $1,800

- You have to apply for at least $8,000 for a vehicle which is eight years old

- Your contact details may be shared with many potential lenders

Best Car Loans by Banks

While there is no denying that banks have been hit hard due to the emergence of many online auto lenders, it seems that the reports of their imminent demise are greatly exaggerated. Because of their sheer size, huge customer bases, and reach many banks are still a big force to be reckoned with in auto financing.

A majority of conventional banks have improved their efforts in order to compete with online lenders and alternative lenders by effectively beefing up direct-to-consumer capabilities while offering the convenient streamlined application as well as approval process as many other online lenders.

Bank of America has long been considered as one of the most suitable car loan lenders among conventional banks in the country. The bank continues to dominate by providing customers with highly competitive rates as well as an easy and quick online application process.

Bank of America is the second largest bank in the US and has a huge footprint with almost 5,000 branches that serve over 45 million businesses and consumers. So, for a lot of car buyers who still prefer the notion of conducting business face-to-face, there is certainly a location nearby. Customers can also apply online to get approval just within sixty seconds and funding can be arranged in just 24 hours.

Also, Bank of America has positioned itself really well as a convenient provider of all loan types, which include loans for vehicles bought from private sellers as well as lease buyouts.

Another great aspect is that the rates are quite competitive when compared with other banks and are very close to the best online car lenders. Also, keep in mind that all current Bank of America customers qualify for interest-rate reductions as well.

The downside is that customer service rankings are not the best; plus, you will not be permitted to take your business to a variety of independent vehicle dealers who sell a number of different makes and models.

Bank of America Pros

- Among the best APRs among all banks

- You will get personal assistance at about 5,000 retail branch locations

- No prepayment penalties or fees

- Easy and quick online application as well as approval process

- Loan discounts are available for both Preferred Rewards and checking customers

- Loans are available for both private party sales as well as lease buyouts

- Bank allows car loans even for higher-mileage or old vehicles

Bank of America Cons

- The bank does not offer financing for car purchases at an independent dealer

- Down payment might be mandatory based on your creditworthiness

- There is no online pre-approval

Chase Bank is one of the four biggest banks in the country, in terms of total assets, and has over 5,100 branches throughout the US. You could visit any branch if you want to apply for an auto loan. You can also go online and get your car loan approved within a matter of minutes.

Chase Bank offers auto loans for as much as $100,000 for both used and new cars; however, keep in mind that a vehicle can’t be over five years old; also, it must have fewer than 75,000 miles.

As you can imagine, auto loan rates tend to vary depending on the kind of car you intend to buy, your credit score, the state you reside in and your loan-to-value ratio. In a majority of states, the most attractive auto loan rate is currently about 2.99% while in other states it is about 2.69%.

Another convenient feature is that Chase offers you an online calculator to allow you to enter information regarding your car, your state, and your credit standing to see the rate you may qualify for. Also, loan rates for used cars start at about 3.09% for high priced models, topping out at about 3.39% for more economical cars.

In order to avail the best APR, you are required to make a down payment. Keep in mind that Chase usually requires a loan-to-value ratio of about 95% for used cars and 80% for new cars.

Chase Bank Pros

- There are no loan fees

- You can avail car loans as low as $7,500

- You will enjoy very competitive APR, especially when coupled with customer discount

- Car search service using dealer discount

Chase BankCons

- There is no online pre-approval

- APRs tend to vary considerably by state

- The minimum loan term is four years

Boasting almost 9,000 branch locations, which give the bank a leg up when it comes to generating new car loans, Wells Fargo certainly has the biggest footprint compared to any other bank in the country. As a car buyer, you can visit your nearest branch and apply for an auto loan or opt for the quicker and easier route by logging in online.

You will be glad to know that Wells Fargo funds most kinds of vehicles purchased used or new from car dealers, independent as well as private parties. The bank doesn’t provide car financing in Louisiana. Although the rates offered by Wells Fargo aren’t the lowest, they can still compete with most other major banks.

Fortunately, loan APRs for new cars start as low as 3.90%. On the other hand, used cars bought from car dealers could qualify for an APR of 4.15%. While the bank offers financing for most private party purchases, keep in mind that the rate is slightly higher at about 6.49%.

According to experts, these are some of the most attractive car loan rates provided by Wells Fargo; however, as indicated on the bank’s website, only a modest 5% of total applicants manage to qualify for them. Also, the maximum rate offered by the bank is 10.51%.

Car loans can be financed for as much as $100,000 and for a maximum term of 72 months. It is worth noting that vehicles older than 7 years are usually limited to a term of 48 months. The lowest loan amount is about $5,000.

Wells Fargo Pros

- You can benefit from same day pre-approval

- Easy and quick online application as well as approval

- Highly competitive loan rates for creditworthy borrowers

- Financing is available for both lease purchases and private party

- Financing is available from as low as $5,000 to up to $100,000

- You can also get relationship discount

Wells Fargo Cons

- You will have to pay an origination fee of $99

- The maximum loan term for vehicles seven years and older is only 48 months

- You will not know the actual APR unless you apply

Loan Types

First determine the types of loan a lender offers. There is a variety of options when it comes to car finance. This includes used car loans, new car loans, refinancing options (where a loan on your existing car could be refinanced), as well as loans for individuals who have varying credit from excellent to poor.

Also, bear in mind that many companies tend to market themselves as sub-prime car finance companies with suitable loan products that can match your needs.

If you look into the different loan types offered by a lender, you will better figure out which companies are the most suitable fit for your specific situation.

Fees

Remember that a number of different fees may be applicable to your car loan. Some of these fees are origination fees, prepayment fees and processing fees. Always inquire about any or all relevant fees on your loan and carefully factor all of them into the costs of your loan.

Interest Rate

Your interest rate will largely determine the amount you will pay for the car over the term of your loan. Note that the interest cost is usually built into your contract and you will pay it as part of the installments. So, make sure you check each lender’s rates for its different loan offerings.

Loan Amount

Consider the maximum and minimum loan amounts that companies provide, as a lot of lenders have restrictions in place.

Term of the Loan

The term of car loans usually ranges between two and five years; however, it could go as high as seven years. Keep in mind that the longer the loan period, the higher you will need to pay as more interest will accumulate over time.

Lenders offer different loan terms, so make sure you check out all the options available to you.

Application Process

The application process is often overlooked, but it is another key variable when choosing your auto loan. You must take into consideration the ease and convenience of applying for your car loan, how long processing will takes and when will you receive the money.

Credit Requirements

With an extensive range of auto lenders, ranging from subprime car finance companies to ones that usually lend at higher rates, verify all of the credit requirements which are set by each lender.

Restriction on Cars

A lot of lenders usually have restrictions in place when it comes to the kinds of cars they will finance; as a result, make sure you check for all the details.

From deciding on the best car to getting approvals for financing, we will take you through the entire online car purchasing process.

It will considerably help to have all your documents ready when you are applying for a car loan. Keep in mind that this includes proof of income, proof of identity, credit and banking history as well as proof of residence.

If you have chosen a specific vehicle, you will also need that information, such as VIN, year, mileage and make and model. And although a lot of online lenders tend to advertise their loan process as being snappy, you should prepare for a few roadblocks. At times, lenders may need additional information or request more time in order to verify specific information, and this can delay the approval process.

So, it is important to be proactive. When you have initiated the auto loan process, your lender would walk you through what is required. However, that does not necessarily mean that you need to wait for your auto lender to get back to you.

In the unforeseen event that your loan process stalls, send an email or make a call and speak with your lender regarding what is needed. The good news is that in a lot of cases, you will have a convenient online login, allowing you to view your loan status, and take the suitable next step online.

Shop for the Loan before the Car

If you visit a car lot and have cash in hand you will have more leverage. Rather than concerning yourself with how you will pay for your car, you will be able to focus on striking the best deal. This is why we strongly recommend you to obtain financing before you shop for the car.

It is best to start with a local bank, or an online lender. You must be aware of your credit score prior to applying for the loan so you know exactly what you can expect in terms of an auto loan rate.

Also, do not make the mistake of comparing rates by advertisements or promotions. It is because those rates are the most affordable car loan rates and are reserved for creditworthy borrowers. A lot of lenders would give you specific qualification guidelines and criteria before you apply for a car loan so that you could see what rate you may be eligible for.

In case you feel you have to apply with multiple lenders, make sure that you do that within a period of two weeks. Also, keep in mind that if a car dealer is providing 0% financing on a model you like, it may be worth considering, given that that fewer than 10% of total borrowers usually qualify for these lucrative deals.

Know Your Credit Score

Always remember that your credit score is one of the most important factors when it comes to what sort of interest rate you could land.

As you can expect, excellent credit scores mean better rates. On the contrary, bad credit scores translate into steep rates – if you can even qualify in the first place. It is vital to know that your credit score may vary by twenty points from one month to another, which can make all the difference between the best auto loan rate available and getting a good loan rate.

A majority of lenders now have simple calculators available that let you plug in your score in order to determine what APR you may qualify for. Always know your credit score and never apply for a car loan blind. You can also use services like Identity Guard or Credit Karma to check your score before you begin shopping.

Look for Discounted Interest Rates

At various times of the year, it is likely that you will come across promotions offered by car dealers for interest rate discounts. These offers could be quite enticing, and, at times, a very good deal, particularly 0% car loans.

That being said, remember that these kinds of loan discounts are often available only to borrowers who have excellent credit; however, they do manage to attract a lot more folks to the car lot. Some lenders may offer you an interest rate discount in case you have a prior banking relationship with them or if you are buying a specific kind of car.

But, it is also vital to keep in mind that car dealers have to make money somehow; therefore, if you fortunately qualify for a discounted interest rate, it is likely that you will end up paying a much higher price for your car.

You can also get a choice between a rebate and 0% financing. In most cases, if you do the math, you might find out that a rebate will cost you considerably less over the loan term with a normal APR.

It is also likely that if you could qualify for discounted interest rate at an auto dealer, you could probably be eligible for the most affordable auto loan rate with an online lender or bank.

In any case, do not assume that you would be told about these potential savings — you should always ask.

Buy New Rather Than Used

In most cases, it is generally easier to secure a more attractive interest rate in case you are purchasing a new car rather than a used one. You will soon realize that average interest rates on used vehicles are considerably higher than new cars.

It is primarily because folks who are looking for loans for used automobiles have much lower credit scores compared to people who are seeking a new-car loan. However, it goes without saying that new cars tend to lose a lot of value immediately after possession is taken, which is a very compelling reason to consider used cars. It is the reason why, at times, they are the best deal for a lot of buyers.

However, always take into account the financing you may secure on a brand new vehicle when you are making this critical decision. For instance, similar sticker prices in case you are comparing a used luxury car and new mid-range car may tip the scales in favor of a new car.

Shorter Loan Terms are Better

In many cases, shorter loan terms come with much lower APRs. Keep in mind that with a majority of lenders, terms of 48 months to 60 months usually offer the best APRs.

In case of shorter loan terms, three years or less, lenders make less money; as a result, they are likely to charge a higher APR than what you may hope for. On the other hand, for longer terms, usually greater than five years, most lenders consider the car loan a much greater risk; thereby, they tend to charge higher APRs. While the monthly payment on a loan term of 84 months term would be lower compared to a loan term of 60 months, note that you would pay substantially more in terms of total interest costs.

The lesson here is that you should never fall prey to an auto dealer who attempts to sell you a vehicle depending on the monthly payment. Instead, you should always look at the APR as well as your ability to repay the loan in about four to five years.

Do Not Use Your Loan to Pay for ‘Extras’

Many car dealers tend to make plenty of money by offering you all the different ‘extras’. You may be familiar with these extras; they may include upgrades such as rust-proofing, security systems and fabric protection, or extended warranties.

A majority of experts contend that buying these add-ons seldom makes sense. However, rolling these extras into the loan makes less sense — it is because the interest means you will pay even more in the long run for these extras. In case there is an add-on that you really need, purchase it separately. Also, consider paying registration fees, sales taxes, and several other tacked-on expenses separately for the same reason.

Think Again about 100% Financing

While many lenders are quite willing to provide 100% financing to a qualified buyer, according to experts it is not a smart move to finance the whole cost of your car. It is mainly because you would likely be upside-down with the car loan, and owe more on the car than what it is actually worth. This can become problematic in case you would like to sell your car soon or you total it in an accident.

So, it is vital to keep in mind that the moment you drive off the car lot, the value of your car will depreciate and continues to do so over time.

On the other hand, if you put 10% to 25% of your personal money down, then you would drive off with some equity in your car, which will increase gradually while you pay down the loan. This way you will have a peace of mind.

Be Careful If You Are Considering a Variable Rate Car Loan

You may have noticed that in the last couple of years an increasingly large number of auto lenders have started to provide variable rates on car loans. Variable rate loans could be very tempting as their APR is generally lower compared to the loan rate on most fixed loans.

Although a variable rate loan may help you buy a pricier car, or even save you plenty on monthly repayments initially, it might cost you a lot more if interest rates increase. Also, if you are considering a variable loan, make sure that you study the maximum loan rate to determine how much your loan rate may rise in the worst case scenario. The only good reason to go for a variable rate car loan is when you have a financially clear plan for repaying it in a relatively short period.

Consider Dealer Financing

This must have crossed your mind. There are actually two good reasons why you may want a car dealer to finance your car. The first being you have lousy credit and need the help of a dealer in securing a car loan. On the other hand, you may have excellent credit and would like to qualify for any special finance offer from a dealer.

Keep in mind that in both cases, financing the car via a dealer can be the best option. That being said, although a car dealer could be a feasible source of financing, you should thoroughly and carefully study their offer as well as the paperwork for any hidden costs or restrictions.

There is no denying that at one time people could, in most case, expect to get a much higher rate on used car loans.

As per this traditional view regarding used car loans, banks and other financial institutions are more wary due to higher risk as folks who purchase used cars tend to have lower credit scores. In addition, used cars may fall into disrepair more often than new cars. Historically, this combination has caused much higher default interest rates on used car financing. But…

Times are Changing

This conventional view seems to be fast changing. This is part because a large number of financially sound and astute car buyers are buying well-maintained and certified “pre-owned” cars, which are almost good as new.

In addition, in the last few years car lots have been flooded by previously leased and low-mileage vehicles. A lot of lenders treat many late model vehicles as new for the purposes of pricing the loan. Although many banks and other lenders still usually differentiate between used cars and new ones in pricing the loans, several competitive online lenders do not, and offer the same low rate on a used car as they do in case of new cars.

Same Process

Usually, the process to obtain a used car loan and a new car loan is the same. In most cases, the lender collects the same information, save that, for used car loans, specific details regarding the age, condition and mileage of the vehicle are also needed.

Also, many lenders now provide pre-approvals in case of used cars, so that buyers can shop for the most affordable car loan rates.

Restrictions

There are often a few restrictions when it comes to the number of miles and age of the car, though some lenders do not have any restrictions. A few lenders treat late model cars (about three to four years old) differently compared to used cars (five years or older).

So, it is crucial to know and understand how different lenders view used vehicles and what type of, if any, restrictions they have on their lending.

Whether you are a car buyer who has perfect credit, keep in mind that there is fierce competition when it comes to getting the best car loan. You should use it to your benefit by doing some comparison shopping prior to signing on the dotted line.

Always look up your latest credit score, consider different loan terms and possible discounts, and know how each piece of the puzzle may impact your bottom line. Consider starting your search for the best auto loan with some of the companies mentioned above, as all of them are great choices.

Finally, another important point worth noting is that the auto loan market is quite competitive, and thereby in a constant state of flux. A majority of lenders usually make changes to their policies and products on a regular basis in order to gain more market share. Therefore, the ‘best’ auto loan on the market may change from one month to another.